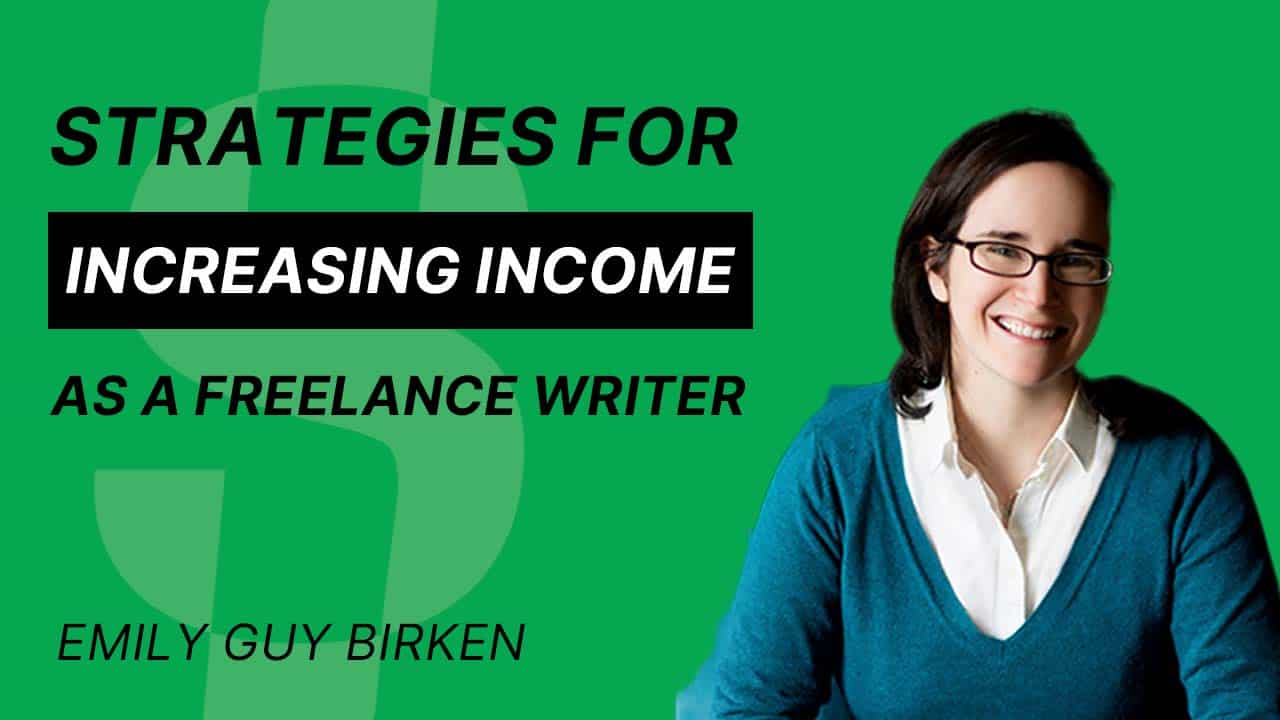

Strategies for increasing income as a freelance writer.

My next guest is a freelance writer with over 10 years of experience, specializing in the field of personal finance, and with a particular interest in the scientific research behind irrational money behaviors. She started her career as an educator and her background in education allows her to make complex financial topics relatable and easily understood by the layperson. Please welcome Emily Guy Birken.

Payback Time Podcast

A Podcast on Financial Independence. Hosted by Sean Tepper. If you want to learn how to escape the rat race, create passive income, or achieve financial freedom, you’ve come to the right place.

Click Here to listen to this podcast on your favorite platform

Key Timecodes

- (00:45) – Show intro and background history

- (04:09) – Deeper into her background history

- (13:41) – Understanding her business strategies

- (19:12) – A bit about her marketing strategies

- (25:34) – How she achieved her financial independence

- (30:23) – How money can buy your happiness

- (37:23) – What is the worst advice she ever received

- (38:44) – What is the best advice she ever received

- (40:59) – Guest contacts

Transcription

[00:00:00.000] – Intro

Hey this is Sean Tepper, the host of Payback Time, an approachable and transparent podcast in building businesses, increasing wealth, and achieving financial freedom. I’d like to bring on guests to hear authentic stories while giving you actionable takeaways you can use today. Let’s go.

[00:00:17.180] – Sean

My next guest shares her inspirational story of transitioning from an English teacher to a full-time freelance writer in the finance industry. In this episode, she talks about how much she charges, how she was able to move from lower paying clients to higher paying clients, and how she markets her services. In fact, she talks about how she is pretty much able to put herself into a position where the leads come on autopilot. It’s a good place to be. This is a fun one. Please welcome Emily Guy-Birken. Emily, welcome to the show.

[00:00:47.050] – Emily

Thank you so much for having me.

[00:00:48.690] – Sean

Thanks for joining me. And just a heads up to the audience, Emily is from Milwaukee. We’ve got somebody else from the Milwaukee area. This is great. Milwaukee represent. Did not plan that. There’s just a network of people out there, a company that connected us that doesn’t even have a location in Wisconsin. And here we are, Wisconsin.

[00:01:08.650] – Emily

It’s pretty awesome.

[00:01:10.380] – Sean

Let’s get right into it. And why don’t you tell us about your background?

[00:01:15.020] – Emily

I am a personal finance writer and the author of five books on personal finance. I did not plan to do this. This was an accidental career. I’m actually an English teacher by training. I taught high school English for four years, and then I tripped and fell backwards into writing about personal finance. So I taught from 2006 to 2010. My oldest child was born in tail end of August 2010, in. And we happened to move from one state to another that summer. So because we’re real good at timing, I was not going to be able to find a teaching job because I’d have to immediately leave to go on maternity leave. So the original plan was I was going to take a year off to stay home with the baby. But then also because we’re real good at timing, we couldn’t sell our house in Ohio, where we’d been moving from. So we went from two incomes to one, two people to three, and one mortgage to two. So it was a little stressful. So because I wasn’t going to be able to teach, I thought I’ll see if I can find some freelance writing that I can do.

[00:02:29.400] – Emily

And one of the first gigs that I landed was for a personal finance website. My dad was a financial planner, so I did grow up in the industry and I’ve always been a bit of a money nerd. And I was like, oh, I can do this. And it took off. So it was very much not the intention of any aspect of my career plan, but it worked out really well, especially since we had moved from Columbus, Ohio, which is not where either my husband or I are from. We met there, but we’re both from the East Coast to Lafayette, Indiana, where we didn’t know anyone and had no family or friends when we got there. And so being able to transition into a freelancing job meant that I could be the primary parent for our child. And I didn’t have to worry about the like, oh, how do we take time off because the baby is sick? Or those sorts of questions like, Oh, we got to get the kid to the well-child visits. That is very difficult when you don’t have a network. So the intention was not for me to continue. The baby turned 13 earlier this year.

[00:03:36.480] – Emily

So the intention was not for me to continue doing this for the next decade-plus, but it turned out that it was a much better fit for both my skills and temperament and needs of the family. And I was able to relatively quickly recreate the amount of money that I was making as a teacher. And so it worked out really, really well for the whole family. So I never anticipated that I would be doing this, but I’m so glad that I did. And I feel like I’m exactly where I’m supposed to be.

[00:04:10.140] – Sean

Thank you for the context there, a backstory. You said you were able to match and exceed salary. How long did that take?

[00:04:17.610] – Emily

Let’s see. So we had our first child in 2010, and then we had our second in 2013. And so it was definitely after our second baby because I ended up taking some time off with our second. And in between all of that, like in that middle time, in between the two boys, the plan still was that I was going to do this and then maybe go back to teaching. And it wasn’t until we were juggling two kids and I was like, I can’t be a teacher. I don’t have two kids. There’s just no way. That I decided to really double down and focus on making sure that I was maximizing my income. Early on, I made a lot of very common freelancer mistakes like jumping at any opportunity, even if it was low pay because well, this could dry up at any time, so I got to take what I can. And accepting lower pay than I was worth, those sorts of things. I had a few clients, none in the personal finance realm, honestly, but I had a few clients who ghosted me and I didn’t get paid, those sorts of things. So once I learned how to navigate those sorts of difficulties.

[00:05:32.700] – Emily

And once I really decided to focus on I want to find higher paying clients and I’m worth it, where can I find those clients? How can I really expand? Is when things really started happening for me. It also helped. It took us about a year. The other reason there wasn’t so much pressure was it took us about a year to sell our house in Columbus, Ohio. But once we sold that house, then my income from freelancing became just like icing on the cake and was no longer like, how are we going to do this? I was clear on the fact that I wasn’t going back to the classroom that I was like, okay, I need to be able to make. My first goal was 50,000 in a year. And once I got there, I started giving myself a higher and higher income goal for the year. And my current goal, I still have not quite gotten there, is I want to outard my husband. All right. So that’s my ultimate goal. I’ve gotten close, but he’s very well paid.

[00:06:38.230] – Sean

Yes, he’s an engineer and he’s been in that space for some time. We’re talking offline about the companies where he works. So, yeah, Caterpillar, correct?

[00:06:50.160] – Emily

Yeah, he has worked at Caterpillar and he’s worked at Honda, prefer not to say where he works right now, but yeah, he’s a mechanical engineer. He is one of the few people in the country who can do what he is able to do. So the upside and downside of that. The upside is he’s always in demand and well paid. Downside is there’s only a few places in the country that needs him. So if he gets a new job, we move. Although I told him with this most recent move, the one that brought us to Milwaukee, I told him, Well, if you get another job, God speed, I’m staying here. I’m not moving again.

[00:07:25.410] – Sean

Sure. Fell in love with the city.

[00:07:28.950] – Emily

I get it.

[00:07:29.400] – Sean

Yes, yes. Long story short, we have a freelance writer here that’s going to exceed the salary of an engineer. Absolutely. You’re an entrepreneur. There’s no limitations. We may talk about a strategy and how to get you there a little bit, but this is good. I like breaking down people’s business models, and then we’ll get into some fun topics here, some of the topics you teach the people you talk to. But with your business model, is it strictly 100 % service-based? Do you do freelance writing or do you have some other, I’m thinking of, like a leveraged income product, like a course or something you sell on a website?

[00:08:06.480] – Emily

So I don’t have a course or anything like that. What I do have is, as I mentioned, I’m the author of five books about personal finance. And so I do get royalties twice a year. I want to make it clear. If you want to become rich, don’t write a book. That’s not… Right. Of the five books, only one of them is generating royalties for me. And that’s just because the way that book sales work, all of that. My first book, it’s called The Five Years Before You Retire, it became an Amazon bestseller very quickly. Never quite got to Wall Street Journal or USA Today or New York Times bestseller lists, but it has had legs that this entire time it came out originally in 2014. I put out an update in 2021, and I earned out my advance with the very first six months it was on sale, which was fantastic. It set the bar high for me, thinking for the next four that came after. But that is something that I have been so grateful for throughout my career that I know at the end of March and the end of September every year, I’m going to get a royalty statement.

[00:09:22.140] – Emily

Sometimes it’s going to be awesome. Sometimes it’s going to be a little bit. But no matter what, there’s a little bit of money coming in. And part of the why I do keep writing books is I believe that this will happen again. And some of my books, they have not yet outearned their advance, but I believe that they will. And so it’s just a matter of time before those start generating royalties as well.

[00:09:44.940] – Sean

What does that mean? Outearn the advance. Can you explain that?

[00:09:48.980] – Emily

Sure. So when you are in the publishing industry, authors are paid in advance for the book that they write. Now you hear about the huge advances like a half a million dollar advance or a hundred thousand dollar advance, most books are going to be much, much smaller. And so my first book, I was an unknown author. The publisher actually reached out to me. They came up with the idea for the Five Years Before You Retire in-house and then went looking for a writer. And my editor was familiar with my work online, thought I’d be a good fit. So that advance was only five thousand dollars, which is very, very small. And you get half of it before you start writing and you get the other half when you’re done. And the intention is this is what will allow you to take the time to write the book. Now, that’s not how it works for fiction. If there’s anyone who’s interested in how fiction writing works, that’s a very different process because you have to write the whole thing and then go find someone who wants to publish it and get the advance. So what the advance is, it’s an advance on royalties.

[00:10:52.050] – Emily

In most cases, authors are going to earn something like 10-15 % if they go through the traditional publishing route. So 10-15 % of every book sold, the author earns. So the advance is the first basically $50,000 worth of books of the five years before you retire sold. Five thousand of that was my advance. And so because I sold more than $50,000 worth of this book in the first six months, I got a very small royalty check. But the first six months royalty check I got a little bit and it was just lovely. It was lovely to get that. But that’s where if you see someone, if they talk about a $500,000 or a $100,000 advance, what that means is the publisher is betting on the book being some huge best seller. So what’s best for the publisher is if they don’t have to pay any royalties because it has exactly earned the advance. They sell exactly $1.25 million worth of books. So the $125,000 advance is paid out and then they’re good. And it’s capturing lightning in a bottle. The publishing industry is bizarre. And you said offline that you really like movies, it’s similar to that where a lot of times publishers are trying to find the book that’s the next Girl in the Train or the next-.

[00:12:27.310] – Sean

Hunger Games.

[00:12:28.220] – Emily

Or- Yeah, whatever. And so you get a lot of things that are very much derivative of something that was huge. And then so it can be tough for someone who has a brand new idea to get it to come out because they’re like, Well, how do we know it’ll sell? Because we can’t compare it to something that has sold well. Those are the sorts of things that go into book publishing and is one of the reasons why if you want to go into writing, you see Stephen King, you see and JK Rowling and Suzanne Collins and E. L. James making millions upon millions of dollars. And those are the outliers. On the other end, you have people barely scraping by. And then in the big middle is mostly you get working writers. And most working writers are going to either be doing something other than writing in addition to the book writing to be able to afford to write their books, or you get people like me who do a lot of freelance writing, and that’s their bread and butter. And then they also take some time to write books, and that also generates some income for them.

[00:13:42.700] – Sean

Credibility boost. We’ll get into that in a second. If anybody out there is a fan of Family Guy. Stooey is always making fun of Bryan. Bryan’s a dog because Bryan’s a writer, yet he’s broke. He’s made no money as a writer. Yes. Yes. That’s the case for most writers. Now, with your situation, you use the book as credibility, and that probably helps you get those higher quality. Because you mentioned that, I want to talk about that a little bit. How do you get those higher quality clients? Because, in other words, your revenue stream is primarily freelance writing then, correct?

[00:14:19.160] – Emily

That’s correct, yes.

[00:14:20.970] – Sean

How did you make that transition from, I hate to say it, the tire-kickers, the bottom-feeders, the people that just they want everything, but they want to pay nothing. How did you graduate from that to higher quality clients?

[00:14:35.410] – Emily

Yeah, that was a bit tough. Now, one of the things that I did early on that I’m very glad of, and it’s long enough ago that the floor sounds really low, but I set a floor for myself, the least amount of money I would be willing to accept. And in 2010, that was $25 for a 500-word article, which is still like even with inflation waytoo low. But I said it because I’d see stuff like where people would be offering $10 or $5 for that amount of work. And so I recognized I have a floor and I will not go below that floor. And so that was one thing that was really helpful. And part of my growth was recognizing when I needed to raise that floor. So that was part of it. Another part of it was understanding what I bring to the writing that no one else can bring. I have a Master’s degree in English education because I was an English teacher, and my undergraduate degree is in English literature with an emphasis on creative writing. I was coming at writing about money from a more literary standpoint, and that gave me a little bit of imposter syndrome early on because I’d have people be like, Well, what do you know about money?

[00:15:59.110] – Emily

I’m like, Well, I know how to research and I know how to write. And I did grow up in the industry, so I have fewer limiting beliefs about being able to understand the stuff than the average bear. But it did mean that if I was looking at an article that was for a rival publication that was written by someone who has an MBA or is some money expert or an economics degree and it was Dry as sawdust, I was like, I can write something that people will want to read even if they’re not deep in the money world. And so recognizing that that was an important thing that I brought to the writing process was really helpful in letting me winnow out the tire kickers, the ones who like, we just need content as quick as possible. I’m like, well, that’s not what I provide. So we’re not a good fit. And so the people who actually did want to, we want to reach out to people who aren’t reading about personal finance. We want to reach the people who need the help. And we need to make sure that there’s personality and warmth and no shaming.

[00:17:10.630] – Emily

I’m like, oh, that’s me. I can do that. But I’m going to cost you. And okay, well, that’s worthwhile.

[00:17:17.740] – Sean

That’s great. I like to hear stories of people like, you don’t want to go for everything. You set your this is the bar not going any lower, whether it’s a project fee or hourly fee or whatever it is you set the bar and you don’t go any lower. Can you share with us a range? What do you charge to write? Do you charge by project or by hour or by article? How do you monetize this?

[00:17:42.010] – Emily

So generally in the online freelancing sphere, you get paid by article. So as I said early on, I was getting like $25 per article. At this point, 13 years into my career, the range is at the low end, $500 for an article, and at the high end, $1500 to $2,000 for an article. Now, the articles that I’m writing now are going to be a lot more involved than the ones I was cranking out for $25 an hour, and I did post back then. But ultimately, it doesn’t take me that much longer. The most recent article that I wrote that was, I think, about $1,500. I had to do two interviews, and not counting the interviews, I think I spent about two and a half, maybe three hours writing. And that’s what I aim for, is I’m hoping to get about if I were to do this hourly, even though I couldn’t do 40 hours a week of writing, my brain would get tired.

[00:18:51.470] – Emily

You’d be exhausted. Yeah. But I’m aiming for an hourly rate of around no less than like $400 for the writing. That’s great. Now, I don’t actually, as I said, I’m not doing 2,000 hours of work in a year at that rate, but that’s what I’m aiming for.

[00:19:11.790] – Sean

No, that’s great. Let’s talk about the marketing aspect. Are they coming to you now because you have the books out or is there still an outreach process or networking schedule you have to adhere to making sure you’re connecting with people, opening doors, letting them know like, hey, I can write articles for you. How do you bring in new clients?

[00:19:34.990] – Emily

So I am very lucky at this point that I have people reach out to me, which is fantastic. The way that I got to this point. Now, part of it is because of that book or the books that I have. So people know me because I’m the author of those books and they’ll reach out to me. But even before that, my publisher reached out to me because they knew my work. And that is all comes back to I go to a conference annually called FinCon. It’s for Financial Media Creators. And I have been going since 2011. I went to the Inaugural FIN-CON. It was the very first one. And that has been such a game-changer. It was at that FIN-CON that I got a client who I was writing a daily column for, and that was the specific work that my publisher knew me from and thought that I would make a good fit for five years before you retire. So that was really fantastic. Just going to this conference on an annual basis, meeting people, letting them know that I’m open for it, and letting them know what I’m an expert in. Because I’ve written a book about Social Security, so if someone’s looking for a social security expert, they know that they can reach out to me.

[00:20:55.130] – Emily

So that’s part of it. Another thing that I think is really important is getting into mastermind groups and socializing with other people in your industry. I am a part of a couple of different writer’s Mastermind groups and have been from the very beginning. Early on, I was in a local mastermind group that was in person when I was still in Lafayette, Indiana. Now all of my masterminds are remote. And one of the things that’s great is that we can talk about stuff like, hey, this new client is offering this amount, but for this much work, does that seem unreasonable or does that seem about right? Or have you had any experience with this editor? And just I want to make a good first impression for my first article. But then we also do, hey, I had someone reach out. They need a writer and I’m full up. Can anyone take this? Can I recommend anyone? And so that has been also really helpful in making sure that opportunities are shared in the industry. And it’s great knowing that I can recommend someone whose work I believe in if it’s a project I can’t take and knowing that they will recommend me.

[00:22:15.830] – Emily

Yeah.

[00:22:16.210] – Sean

I’ve had multiple guests on the podcast recommend Mastermind groups or networking groups of some sort. In many cases these days it’s online, fortunately, because COVID put us in a fast forward with like, you use Zoom and Teams and and Google Meetup or whatever as much as you can. So yeah, that’s a good call. Now just brainstorming here. I’ve seen people in your position that are an author and then they provide a service. And an in-between product that might create some passive income would be a course that I don’t know if you probably already thought of this, but that teaches other writers how to get more clients. Because the biggest challenge you run into really any business is marketing and sales. How do I get better at marketing and sales? So just food for thought. If you wanted to level up your income, you already have the books. You might have a way to get a lead funnel or a lead magnet with additional material for free, get them on an email list, and then you can sell courses or a course thereafter.

[00:23:20.550] – Emily

I’ve actually looked into that multiple times, and I had a realization recently. I was listening to a podcast where they were talking about the bank robbery that led to the term Stockholm syndrome. And so they were talking about all the work that the heisters, the robbers did prior to and then everything going wrong and dealing with the hostage situation and all of that. And in my head, I was like, is that really easier than a nine to five? The amount of work that you have to go into to live a life of crime and to rob a bank. And it clarified something for me, which is that any time I’ve looked into doing that marketing that leads to a funnel that leads to something that would be more passive income for me, I shy away from it because in my head, I’m like, that sounds like work.

[00:24:12.850] – Sean

I don’t want to rob a bank.

[00:24:15.680] – Emily

I’ll just go do this. I would rather work at the bank than rob it. And so recognizing… And so some of that is at some point I suspect I’m going to get to a point where I am going to need to level up. And when I get there, it’ll be partially because I have gotten to the revenue point where I can hire someone who can do the work that I don’t want to do, which I’ve already done. I have a virtual assistant who helps me with my email newsletter. When I write blog posts from my website, I’m happy as a clam to write them, but actually getting them posted with the images and formatting and links, it’s just like, Oh, it sounds like work. But that’s something that I’ve slowly been embracing the idea of if I am hesitant about doing something, I do need to push enough to know if it’s not just like imposter syndrome hesitancy or if it’s my brain going, no, I don’t want to do that. I would rather get another $2,000 article and honoring what it is my brain wants to do, what while also not allowing myself to stay too close to my comfort zone.

[00:25:34.090] – Sean

Right. If you want to, and if we’re going to have fun here, you want to surpass your husband’s salary, this is your ticket. I’ll put it that way.

[00:25:43.180] – Emily

A lot of- Oh, yes, I do understand that.

[00:25:45.990] – Sean

Yeah, the passive income. Now, the correct approach, and I’ve been researching how to do courses the last 10 years plus, finally executed on a year ago, and it’s paying off. Usually, the best way to go is don’t engineer it. Really lean on your audience. Ask them what are the biggest pain points you have, and then address those and start small. You can start small, keep adding to the course. And of course, you can level up your prices in the course as more content is added. But just lean on them. Let them do the hard work. And they’re not really doing hard work. It’s just like, usually as an entrepreneur, you’re thinking, I got to come up with that big idea. It’s like, no, you do not. Ask your customers the biggest pain point. You can even start with a live course. I’m actually doing that. Coming up soon with the second course, I’ll start live and then chop it up into bits and put it on to… I use Teachable. There’s plenty of platforms out there. Teachable just seems to be the right price for all the features I wanted. But anyway, it is a great bolt-on to a service or another product you have.

[00:26:53.760] – Sean

I don’t always love when I hear somebody, their only business model are courses because it reminds me of 2013 when you have the guy teaching people how to create courses. I created a course on how to… I think of pyramid schemes or the snake eating its own tail, like we’re just round and round on this. It’s like, no, it should complement something you’re already doing. And to me, it seems like a shoe in. And you’ve got a VA. If you wanted to do video, you got to upwork, find somebody who’s really talented, can chop up some videos for you for pretty low price. You find the right people, you can put it together in no time.

[00:27:32.590] – Emily

Yeah. And it is something I’ve dipped my toe in a few times. And because I am at a point where I feel very confident in my freelancing career and in the royalties that I’m earning, I am actually going in directions that I feel exciting to me. My sister and I just recently launched a podcast where we take deep dives into pop culture because we both really love overthinking stuff, and we were both English majors. So it’s called Deep Thoughts About Stupid… I don’t know if I can curse.

[00:28:11.020] – Sean

Please do.

[00:28:12.000] – Emily

Deep Thoughts About Stupid Shit. And so we look at stuff like Twilight, Ghostbusters, The Princess Bride, Neverending Story. Yes. And in each episode, we talk about some major aspect of pop culture and really dive into what are the themes and messages that we took in with this pop culture that we didn’t realize we were listening to and had created furniture in our brain. And so that’s the thing where I decided earlier this year we were going to go all in on this rather than something that would maybe complement what I do with the personal finance and the writing more just because it sounded so fun and brought so much joy to both of us. And so it’s one of those like, okay, we’re going to start small with that and see if we can grow that to the point where that is bringing income in a consistent way.

[00:29:09.320] – Sean

I love it. Now I did hear, I got to throw a flag on the play here. I heard Ghostbusters mentioned in the list, and there’s nothing stupid about that movie. No, I’m just kidding.

[00:29:19.440] – Emily

That’s one of the things that we say over and over again is we call it that because so many people will say, Oh, it’s just pop culture. Don’t take it so seriously. We’re saying, No, just because it’s popular and doesn’t mean that it’s not worthy of our love doesn’t mean it’s not worthy of our overthinking and analysis.

[00:29:41.250] – Sean

I love it. I’ll check it out. You’ve caught my attention.

[00:29:45.440] – Emily

Well, thank you.

[00:29:46.530] – Sean

Let’s take a quick commercial break. Hey, this is a quick heads up that we have a second podcast titled TopStox. With TopStox Podcast, I talk about investing, business, and finance. The audio content is published on your favorite podcast platforms such as Apple, Spotify, Google, or Amazon. The video content is published on the Tykr YouTube channel, so you can either watch or listen to each episode. These episodes are just me, so no interviews. The overall goal is to help you become a better investor. Go ahead and look up Top Stocks Podcast or check out the Tykr YouTube channel. All right, back to the show. All right, before we jump to the Rapid Fire round, I want to ask you one fun question I found in your marketing material, which was actually money can buy you happiness. Here’s how. Can you explain that?

[00:30:37.400] – Emily

So we tend to have these really strong views of money that are very shame-based, where the best things in life are free and money can’t buy happiness. But at the same time, we’re bombarded by these advertisements where you’d be happy if you had a Tesla, a boat, Coca-Cola, whatever it is. And so recognizing that actually money does help you feel happier if you spend it in the right way. And so there is some really fascinating research into what our brains do when it comes to anticipating pleasurable experiences and how we enjoy them at the time and how we look back on them. And one of the things that they have found is that our level of happiness is better predicted by our day-to-day levels of contentment and annoyance than they are by anything really big. So everyone feels great on their wedding day, or I hope so anyway. Everyone feels great on a vacation in Greece, but that is a momentary thing. And if you put all of your happiness eggs in that basket, you forget about the the annoyance and the stress of planning the wedding or planning the Greek vacation. You forget about all of the day to day issues that can make it difficult to get to that very happy day.

[00:32:11.850] – Emily

And then because of something called the Hedonic adaptation, once you get to that wonderful day, it gets to be normal. So it’s not so much the case with a single day like a wedding day. But your two-week vacation in the Greek Isles by day three, you’re used to it. So what that means is the way to derive the most happiness out of your money, out of your spending, is to spend on regular small indulgences that you will always enjoy. So, for instance, going to a happy hour with your best friend every week is going to be a lot more satisfying and give you a lot more happiness than if you were to save up that money and go for a weeklong spa vacation with your best friend. You’re going to have a lot more joy from that weekly repetition. Similarly, I am someone who I love like stationary. I love pens and markers and things like that. And regularly spending a little bit of money on something that I enjoy is going to feel better than buying a new car. And it’s because I get a day to day satisfaction out of it rather than whereas the new car before the new car smell has dissipated has become old hat, and it’s just my wheels and how I get around.

[00:33:39.470] – Emily

Those are the sorts of things that we don’t really think about because we think about money as being like a big, splashy thing. That’s what makes you happy. And it will for a very short period of time. But if you want ongoing happiness, spend a little bit of money on regular purchases, usually experiences are going to be the best ones that consistently make you happy and are something you look forward to.

[00:34:06.710] – Sean

I love that. This type of behavior on money is very similar. You probably know the guy Dan Ariely.

[00:34:13.340] – Emily

Oh, I love him. Yes. Yes.

[00:34:14.970] – Sean

The psychology of money and these simple things you can do in your life that just brings so much more joy. He doesn’t teach exactly what you just talked through right now, but it’s in the same vein. I’m curious, is there a particular book in your list of five that really speaks to this the most?

[00:34:33.410] – Emily

Yes. My book, End Financial Stress Now, is about how it’s inevitable that we will all have money stress, but a lot of the money stress that we have is completely unnecessary. It’s something that we put on ourselves. And so the book is entirely about letting go of limiting beliefs about money and recognizing what are actual money problems and what are problems that we are assigning ourselves just because of the way that we have been taught to look at money, the way that we have grown to look at money. And so that book, I absolutely loved writing it. It was and I had had it in mind for about eight years before I wrote it, and is very much about creating a money situation for yourself that is going to reduce your level of stress and letting go of stressful assumptions that you might have about money.

[00:35:34.670] – Sean

Right on. I’m adding it to my Amazon shopping cart as we speak.

[00:35:38.260] – Emily

Oh, thank you.

[00:35:40.500] – Sean

Awesome. All right, well, let’s jump into the rapid fire round. This is the part of the episode where we get to find out who Emily really is. If you can try to answer each question in 15 seconds or less.

[00:35:51.280] – Emily

You ready? Okay.

[00:35:52.220] – Sean

What is your favorite podcast?

[00:35:55.210] – Emily

If books could kill with Michael Hobbs.

[00:35:58.580] – Sean

Okay, niceAll right. What is a recent book you read and would recommend?

[00:36:04.040] – Emily

The Lamplighters by Emma Kodex, I believe was her last name. It’s a just phenomenal story about three Lighthouse Operators in the 70s who disappear. It’s based on a true story. These three men just disappeared. They have no idea what happened to them. And it tells the story in two parts: the days before they disappeared and then 10 years later, the three and how they have moved on from that moment.

[00:36:34.310] – Sean

Is this a fictional story?

[00:36:35.840] – Emily

It’s fiction. Yes. Okay, sounds my theory. It’s based on a true story, but it is fiction. And it stuck with me for just weeks and weeks and weeks. I’d find myself thinking about it again.

[00:36:46.710] – Sean

The Lamplighters of?

[00:36:48.680] – Emily

The Lamplighters. And the author’s name is, I believe, Emma Codex.

[00:36:52.650] – Sean

Very interesting. I love mystery.

[00:36:55.690] – Emily

The rippler, suspense.

[00:36:58.020] – Emily

That’s my catnip, is when they’re like, We have no idea what happened to them. And the door was locked. I need that.

[00:37:05.120] – Sean

Well put. All right. Movie question. What is your favorite movie?

[00:37:09.360] – Emily

The Big Labowski.

[00:37:11.230] – Sean

The dude.

[00:37:13.570] – Emily

I taught my children to say, careful man, there’s a beverage here, when they were four.

[00:37:18.800] – Sean

Donnie, we’re out of your element. That’s so many good lines. All right. What is the worst advice you ever received?

[00:37:28.050] – Emily

I was told our first house my husband purchased before he and I got married. He purchased it by himself. And it was in 2005 when they were throwing bags of money at anyone with a pulse. And so he only put a very small down payment. But the rest of the down payment was a home equity line of credit, basically. And so when we got married in 2008, I was uncomfortable having this. I mean, he was continuing to pay it, but I was uncomfortable having it. So I was like, how about we live on your income and we’ll use mine to pay down that loan? And someone who was in the financial realm told me like, well, that’s stupid. Why would you do that? And It’s unbelievable. Think she was like, you want to keep that line of credit open in case you want to do renovations on the house. But it was like, it’s a both ends. We can do that. And what? Because she was in the financial realm, I was like, Are we doing something we shouldn’t be doing? And I did a little bit of Googling to be like, does this make sense?

[00:38:37.010] – Emily

And decided to just go with what we were doing because it felt good. And I’m very glad we did.

[00:38:43.690] – Sean

Right on. All right, we’ll flip that equation. What is the best advice you ever received?

[00:38:49.030] – Emily

It was actually when I was pregnant with my eldest. I was taking a water aerobics class at our local YMCA. I was the youngest person there about like 20 years. And I was remarking, I was about seven months along. I was remarking to one of the lovely, motherly women who exercised with me that I was nervous about being a mom. And I’ve always been a straight A student, get the gold star. Am I going to do this right? I’m scared I’m going to screw it up. And she said to me, Well, he’s never had a mother either. So as long as you keep him safe, there are no rules. And that was so helpful for me in terms of parenting. Absolutely. But it has also helped me in other areas of my life, like becoming a freelance writer because I was just like, Well, am I doing this right? And at the time, blogging wasn’t brand new, but it was still pretty new. And I’m like, Is this real writing if it’s not in print? And thinking like, Well, this hasn’t happened for anyone else either. So why do you need… There are no rules that you have to follow.

[00:40:01.880] – Emily

As long as you’re doing right by your clients and doing right by your family financially, go for it. Do what works.

[00:40:10.220] – Sean

Right. I love that. Great advice. All right. And last question here is a time machine question. If you could give your younger self advice, what age would you visit and what would you say?

[00:40:20.150] – Emily

Oh, goodness. I think I would go back to my 20-year-old self, and I tell her to… I’d probably give her similar advice. It’s okay. You can make it up as you go along, and no one’s paying attention like you think they are. I don’t think she would have listened to me, but I think it would have been great if I could have internalized that back then.

[00:40:53.340] – Sean

Yes, I totally get it. Our younger selves knew everything. Oh, yes. So they thought. So they thought. Cool. All right, Emily, where can the audience reach you?

[00:41:03.430] – Emily

So you can find me at my website. It’s emilygyberken. Com. That’s E-M-I-L-Y-G-U-Y-B-I-R-K-E-N. Com. I am also still on Twitter. I don’t know how much longer, but my handle is @emilygyberken. But that’s also my handle on Threads, Blue Skye, and Instagram, and also TikTok. So if you’re hoping to find me, use that handle on whatever social media you’ll probably run across me.

[00:41:33.550] – Sean

Awesome. We’ll get all the links posted below, but thank you so much for your time. This was a blast.

[00:41:39.370] – Emily

Thank you so much for having me.

[00:41:40.900] – Sean

All right.

[00:41:41.470] – Emily

We’ll see you. See you. Hey, I’d.

[00:41:43.170] – Sean

Like to say thank you for checking out this podcast. I know there’s a lot of other podcasts out there you could be listening to, so thanks for spending some time with me. And if you have a moment, please head over to Apple Podcast and leave a five-star review. The more reviews we get, especially five-star reviews, the higher this podcast will rank an Apple. So thanks for doing that. And remember, this show is for entertainment purposes only. If you heard any stocks mentioned on this podcast, please do not buy or sell those stocks based solely on what you hear. All right, thanks for your time. We’ll see you.