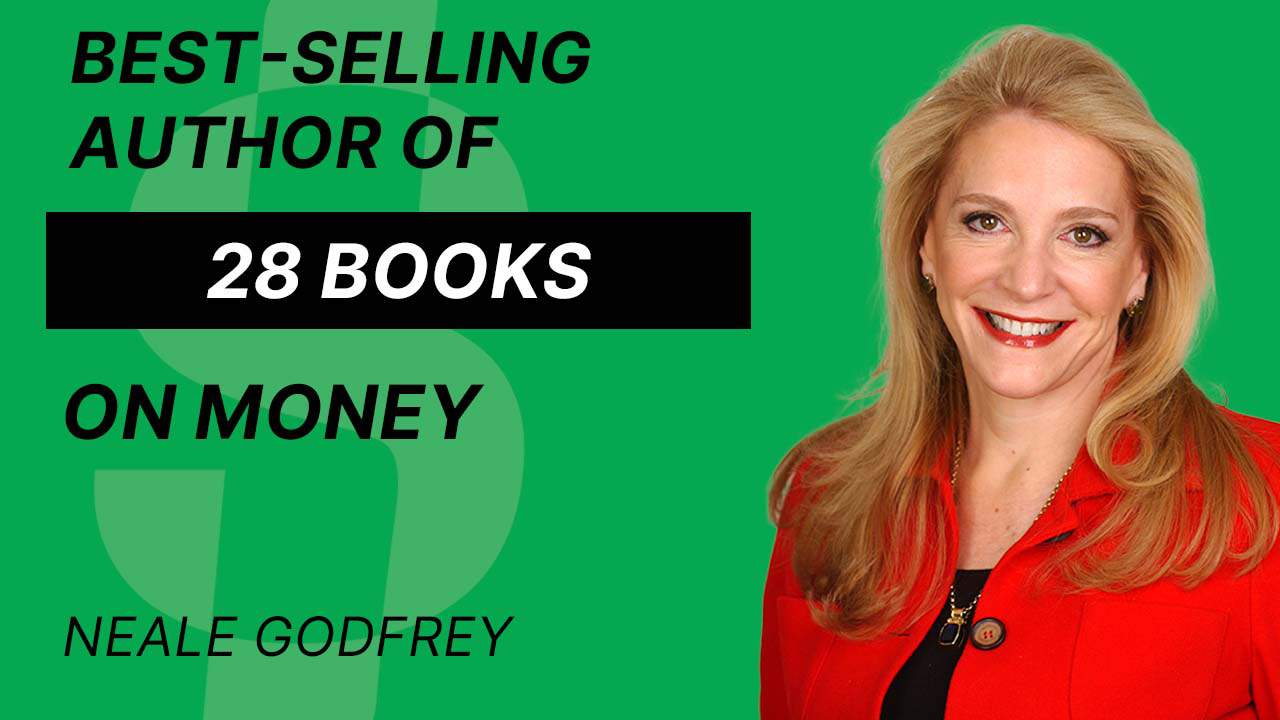

Neale Godfrey – Best-Selling Author of 28 Books on Money.My next guest has about 6 decades of experience in finance and shares her story of becoming an executive in the early 1970’s when women leaders in business weren’t common. She then shares her humble journey of becoming an author and eventually writing 28 New York Times #1 Best selling books on Money, which led to being featured on Oprah. She has a passion for helping families, especially children, become more knowledgeable about money. Please welcome, Neale Godfrey.

A Podcast on Financial Independence. Hosted by Sean Tepper. If you want to learn how to escape the rat race, create passive income, or achieve financial freedom, you’ve come to the right place.

Click Here to listen to this podcast on your favorite platform

Key Timecodes

(00:59) – Show intro and background history

(07:29) – Deeper into her background history and career journey

(09:06) – Understanding her financial educational background

(11:18) – A bit about her first book “Kids Money”

(14:09) – Some takeaways about children, money and financial education

(17:36) – Understanding the custodial account strategy

(19:00) – A bit about her financial education app

(23:30) – A key takeaway from the guest

(27:23) – What is the worst advice she ever received

(27:35) – What is the best advice she ever received

(28:53) – Guest contacts

Transcription

[00:00:00.000] – Intro

Hey this is Sean Tepper, the host of Payback Time, an approachable and transparent podcast in building businesses, increasing wealth, and achieving financial freedom. I’d like to bring on guests to hear authentic stories while giving you actionable takeaways you can use today. Let’s go.

[00:00:17.370] – Sean

My next guest has been working in finance almost the last six decades. She actually shares her story of how she worked her way up in executive leadership in the early 1970s, which was very rare for a woman that’s an inspiration to the story. She then talks about her story thereafter of moving into her career as an author, which was quite a rocky road, but eventually led to her writing 28 bestselling books, and she was even featured on Oprah. Now, today she spends a lot of her time helping families as well as children become more knowledgeable with money to really set up those kids with a strong financial future. If you’re looking for another episode that’s really focused on money and kids, this is a good one, please welcome Neil Godfrey. Neel, welcome to the show.

[00:01:01.510] – Neale

Great to be here, Sean.

[00:01:02.980] – Sean

Yes, thanks for joining me. Why don’t you kick us off and tell us about your background?

[00:01:06.750] – Neale

Well, basically, I was one of the first female executives in banking in the United States in 1972 when Chase Manhattan Bank decided to take a big risk and hire a woman to become an executive. I rose through the ranks, became an executive. Oh, and Sean, this is interesting. I was hired at the same rate, the same amount of money as the men going through the training program. Again, 1972, it was $11,000 a year. I know that sounds ridiculous, but that was actually a good salary in those days. And after two weeks, the head of personnel called me into her office and said, You’re a woman. You’re taking the job of a man. We’re going to reduce your salary to $6,500 a year. And she informed me, You will never earn what the men are earning because you’re taking their job. She was true to her word. I only highlighted it because it’s such a different time that we live in, which is great. Anyway, rose through the ranks and actually was lucky enough to put together, in 1980, the largest merger in the history of the United States, which was the Dupont-Connoco merger. First time we did billions.

[00:02:21.080] – Neale

It was cool to be able to put together that deal. I actually reported into David Rockefeller because it was a secret deal that we were being able to fund. Then I left. I hit the glass ceiling. 1985 I left. I was a single mom of two kids and became President of the first woman’s bank. We needed a woman’s bank because the Fair Credit Act had not been enacted until 1974, and that meant that women could not get credit on their own name. I know it sounds goofy, but my first credit card at Chase Manhattan Bank had my then-husband’s name on it. He had no credit. He was a law student. I was the executive at Chase, but I wasn’t allowed to have my own credit card. Isn’t that crazy?

[00:03:12.370] – Sean

That’s crazy.

[00:03:13.280] – Neale

I know it’s crazy. Anyway, I just highlight that stuff because we’ve come a long way. Not there yet, but we’ve come a long way. Anyway, I saw women at the first Women’s Bank disempowered handling their own money, and that seemed crazy. I did research, and it was because we were never taught anything about money as kids. I went to look for books to teach my own little kids about money, and there were none. The topic of teaching kids about money did not exist in the 1980s. After I had slept my kids to enough stores, my three-year-old daughter said to me, Mommy, why don’t you just write the books? I was taken aback. I knew how to be a bank president and do big deals. I didn’t know how to write a book. She saw that look on my face and said, Oh, you’re afraid. So being the great mom I was, I crouched, established eye contact with my three-year-old and said, Now I’m not afraid. But of course I was. I had no idea how to start a new topic, how to write a book, whatever. I figured it out, wrote a book called The Kids’ Money book to empower children to take charge of their own financial life, to be financially independent, and to work with their parents and schools to make sure that we were raising financially literate children.

[00:04:38.560] – Neale

Went into Simon & Schuster, largest book publisher in the world, and said, Tada, we can educate kids all over the world. Their reaction was, There are no books to teach kids about money. Thanks for stopping by. It’s not a topic of interest. I was banished to the streets of New York, crying, holding my manuscript. Then it was, Oh, come on, put your big girl panties on. They need proof of concept. I opened up the first Children’s Bank at FAO Schwartz, the toy store in New York, a real bank for kids in 1988. Princess Diana flew over with the Royal Children to open up accounts at my little bank, which was pretty cool. I also opened up an institute for youth entrepreneurship up in Harlem to work with at-risk kids, bring them into the economy. Both were successful. Back to Simon and Schuster. Simon & Schuster said, Okay, this is cute in terms of what you’ve done, but there still are no books to teach kids about money. We’re not going to take a risk on a new topic. Back to the streets of New York, back in tears, and then the conversation with myself again, put your big girl panties on.

[00:05:49.040] – Neale

You knew you know how to buy and sell companies, so I bought a publishing company. I bought a division of Macmillan under the proviso that obviously they would publish my first book. I informed them at our first publishing meeting that I would fire everyone if they didn’t publish my first book. They made the miraculous decision of publishing my book, published it. We sold 50,000 copies. I sold the publishing company and went back to Simon & Schuster, who now would take me on as a property. Then the phone rang one day. My daughter picked it up. She was now 10 years old and she said, Mommy, Oprah is on the phone. I said, No, it’s not Oprah. I have a friend who does Oprah impersonations. Give me the phone. I was a jerk. I did Oprah to Oprah climb every mountain. I was singing. I was being a jerk. My daughter held up a piece of paper that said, You can ruin your life, but don’t ruin mine. It’s Oprah. Cut it out. It was Oprah. I worked with Oprah for four and a half years. I did 13 shows. That book hit number one on the New York Times bestseller list and the rest is history.

[00:07:02.370] – Neale

I continue my work today. I just finished my 29th book, which indicates I have no life and created the first money curricula. I’m an executive in residence at Columbia Graduate School of Business. I’ve been on the board of UNICEF, UN Women. I work with wounded veterans out of Syracuse University, yada, yada, yada, and here we are.

[00:07:29.820] – Sean

Sure.

[00:07:30.200] – Neale

I’m thrilled to be here with you.

[00:07:32.120] – Sean

Love the backstory. That’s fun. Now, 29 books I saw I was reading online 28 books, but 29 books on… Is it really focused on finance for kids or has it spread out a.

[00:07:44.880] – Neale

Little bit? No, it’s morphed. I combined ecology into some of my teachings, and I have a program called the Echo Effect, the Greening of Money, because the saving of resources is the same behavior as saving money. And so if we combine, if you save energy, you also save money. So that mindset and that comes with curriculum, et cetera. I also have another program called Life Inc, the ultimate career guide for young people. The purpose of that is to engage young children at age 10 and above in thinking about their future. Because if you can see your future, there’s a reason to stay in school and learn today. The latest book, I also have books empowering women to take charge of their financial life. The latest book that will come out in July is called Get Off Your Assets. It’s designing a guide for women to design their gray divorce. Gray divorce is divorce over 50. That’s the largest segment that is growing in the divorce field. Women are actually initiating those divorces, and they need help navigating finances. So we can talk about that in July.

[00:09:05.180] – Sean

That sounds good. All right, so let’s talk about kids and money. I have talked to other people on the show that really focus on that as well. It still seems like it’s crazy. You started getting into this into the 1970s, and here we are, 50 years later, going on 60 and still not a large emphasis of financial education for kids specifically like how to increase income, how to create more streams of income, and how to use compound interest in your favor. That’s what we’re all about here at Tykr. Could you talk about that a little bit, how it’s not really evolved as much as you’re making a dent, but the whole industry is not moving as fast as you would expect it to.

[00:09:52.310] – Neale

There are a couple of reasons, Sean, for that. Typically in the United States, our Puritan values were that polite people don’t talk about money. There’s still a hangover on that. And what that has affected is that the core standards in our country do not include financial literacy as a core standard that’s going to be… That the kids are going to learn and that they’re going to be tested on. So when it’s not part of core, it’s really difficult. I did the first lobbying efforts and actually got the state of Ohio to agree to even teach. This is back in the ’80s, and it was like a novel approach. The curricula that I had to create is what we call supplementary, meaning it can slip in during the school day if the teacher wants it. I also went to after-school programs because it was important to do it. I’ve gone under, over, and around the side. But until we, as a country, understand that unless you have a seat at the economic table and understand what you’re saying in terms of compound interest and wealth building, you will not be part of the conversation. I know that’s harsh, but the fact of the matter is unless we empower our youth to build net worth, to do that, they’re always going to be disempowered.

[00:11:18.650] – Sean

Right on. Okay. What I want to do is touch on that first book a little bit, and then let’s touch on maybe the recent. The first book, let’s go deeper into it. This was the first one you had a hell of a time getting this out the door. But let’s go into that book a little bit.

[00:11:35.370] – Neale

The Kids Money book was written, and it’s been redone and upgraded to the ultimate Kids Money book. Basically, I create cartoon characters called The Green Street Kids. The reason I did that is so that young children would identify with these characters. We are connected, as you know, Sean, by our financial personality, meaning how we handle money, not our socio economic level. We’re savers or spenders, and we come to the world that way. The characters were based upon financial personalities. Of course, if I’m going to write my own books, I have Penny Bright, today’s savvy, feline, and entrepreneur, and she knows her fashion and her tax code. And then there’s dollar, Bill Buck. He wants to save his money. He gets his attention diverted. There’s Anna Budget. She’s a smart shopper. She’s a squirrel. There’s Hedge. She Hedges her bets. And they’re the Market Brothers, Bull and Bear. And they run the Blue chip deli in Green Street Common, which is where the characters live. And sometimes they cook muffins and buns and sometimes they burn the buns and they throw them out and they call them junk buns. But anyway, so what I try to do is also demystify terms for people because as soon as you know, you throw a term out, a convertible, subordinates, made a adventure, you lose your audience.

[00:13:02.580] – Neale

So it’s to demystify, make things very simple. And I teach earning, saving, spending and sharing. I start at age three and I take them all the way up and I teach them to invest. I teach them to make sure that part of what they’re doing is first saving, then investing. And charity is a very big tenant to in terms of making sure that it’s not just about yourself. I also teach the kids that to push off instant gratification and save for something larger. I make it simple. I make it engaging. And that’s what my books do. I teach the parents at home, the kids at home, the kids at school, and the kids after school. I try to engage corporations and not-for-profits who share my mission and financial advisors who want to make sure that they’re bringing this information to their clients so that their next generation is also learning this stuff.

[00:14:08.920] – Sean

Right on. We’ve got listeners in our audience that have kids that are, can be teenagers, but there’s a good majority that have kids that are pretty young. We’re talking like 2-5, 5-10, somewhere in there. What are some great takeaways you can give those parents right now?

[00:14:26.970] – Neale

The only way to get money is to earn it. There’s no entitlement program out there. It’s just not hitting up mom, dad and grandma, grandpa, can I have a 20? Can I have this? Can I have that? What I do is I start the kids on a very simple work-for-pay system within the household. Kids at age three, if you ask them, What do mommy and daddy do with money in a store or a credit card? They will say they buy things. That’s the time to start connecting how you get the money. I have them do very simple chores around the house. They earn their money, and then they budget it, and they budget it very visibly. I know we’re in the world of digital money, but I want you to start tactile, so kids understand the connect between this is money. It goes into the bank, then it becomes digital, and then they start to not confuse money with digital games where you’re buying moons and stars and benefits, which is all digital and it’s gaming and it’s not real. I want them to understand real, then you move into digital. In the budget, there’s some instant gratification.

[00:15:40.660] – Neale

I call it quick cash. They’ve worked hard. They get to make some decisions. Then there is the charity, JAR or Envelop, which is 10% to give to charity. Then they pick a goal for medium-term savings. They push off instant gratification, save for a little bit, understand that you get better stuff if you save a little bit, and then there’s long-term savings. That is for the little ones saving and for the older ones by age 10, they can start getting involved in investing in the stock market, obviously through parents. You’re going to say, does a three-year-old understand long-term savings? No. Does a 10-year-old understand long-term savings? No. Do the adults in America understand the concept of long-term savings? No. You do that for a living. You know that. I’m just forming a habit. A budget is a habit. That’s what I basically do within the household.

[00:16:44.140] – Sean

Got you. Is there a particular book on your list that speaks to some of the tactical strategies you spoke to just now?

[00:16:50.410] – Neale

Yeah, there are two that you could… There are several, but Money Doesn’t Row on Trees is on Amazon and The Basic Tenants for little ones, school-age and then older teens and Young Adults and also Be Money Smart in Tough Times, which is my latest book that I did in COVID. And it’s also got the same basic tenants and it brings in some of the digital aspects of this. Those two books are there. Excellent. They’re a bunch of others, but obviously.

[00:17:24.460] – Sean

Great. Yeah. We always start small with the call to action. People can get one book and then go to another and go.

[00:17:32.010] – Neale

To another. Yeah. They can book leave and they can just go on Amazon and buy books.

[00:17:37.910] – Sean

That’s great. Love what I’m hearing so far. Do you talk about it in your books at all about setting up a custodial account? I’ll talk to my audience about that a little bit. The parent can work with the child, set up a custodial account. I’m just helping out the audience here if they don’t know already. But when the child turns 18, then they get that account. But under the age 18, it’s like the parent can manage it with the child.

[00:18:03.670] – Neale

Yes, the answer is yes, and it’s important. If you raise the kids with the values and life skills that you want them to live in the real world with, then you don’t have to be afraid of the fact that at 18, the money legally becomes theirs. And if they want to buy a Ferrari instead of going to college, they actually legally can. It takes a lot to step in, as you know, to change that paradigm. But the parents I work with, and I’m sure the ones that you work with aren’t worried about the Ferrari. The kids understand. It can, as you know, if you think you’re going to qualify for student aid, the money, because it’s legally the kids, can count against them when they’re filling out the financial aid form. That’s just something to think about. If you’re going to be on the cusp of that, don’t. But if you’re above it, it doesn’t matter.

[00:19:00.940] – Sean

Sure, right on. Good advice. Let’s talk about this app you created. I’m reading here, number one educational gaming app teaching kids about money. What’s the name of this app?

[00:19:12.620] – Neale

It’s called Green Streets, Schmuths, Happens. Now, what happened was, however, I took it down from Apple because they were charging me $50,000 a year to keep it alive. I’m actually looking for a corporation who wants to license it and we can regenerate it. It’s really fabulous. It had an average playing time of over an hour for the kids. We did hit number one on Apple Education. It really teaches the kids the earning, saving, spending and sharing and pushing off instant gratification to see how their money in the bank can actually earn an interest. So it’s really cool. But yeah, so I need somebody who’s there to go, ta-da, want to work with you.

[00:20:05.330] – Sean

You know what’s interesting? Because I just got off a call. Do you know Scott Donnell? He was just on the podcast a few weeks back and he created an app called Gravy Stack that it goes over seven principles such as savings investing. I think it’s savings earning. I don’t know. Sorry, Scott, if you’re listening to this. But it talks about earning savings, giving to charity, investing. And it sounds very similar, and this app is out there. It’s cartoony, very appealing to kids, and parents can manage the activity on it. And you’ll like this, and you just talked about this a little bit, is creating incentives for kids to earn money within the household. What he would do is talk a little bit about how you can get rid of stuff, like run a garage sale, like a pop-up garage sale, and sell some stuff you haven’t touched in three years, and make a few hundred bucks, little things like that.

[00:21:03.570] – Neale

Right. Now, and that’s all stuff that my work dating back to the ’80s. So that’s great. I love when other people jump in and do derivative work based upon my stuff. It’s great. It’s what I wanted to do.

[00:21:22.250] – Sean

I’ll make a connection off the call. I think it’ll be good for you two to talk. I’m really passionate about this, is getting ahead of it, because I wish at age 10, I would have knew how to invest. Where I’d be, it’d be totally different. But yeah, kids can get way ahead of it if you learn how to save and how to invest at a young age, use the power of component interest. This stuff is fun. Let’s touch on what is your most recent book titled?

[00:21:51.210] – Neale

The Money, Smart and Tough Times. Okay. Coming out of COVID and having people really look at their own situation vis-a-vis their children and what that means. It’s a book for parents and grandparents. It just came out last year and obviously incredibly relevant to what’s going on in our world. Again, based upon the values that you want your kids to live by.

[00:22:21.760] – Sean

Yeah. Awesome. Let’s take a quick commercial break. Investing in the stock market. I’m sure the top questions that come to mind include how is it? And can I actually make money? Every day people like you or I, or otherwise known as retail investors, are flooding to the stock market because a friend told them, or maybe they saw something on YouTube, heard something on a podcast, or maybe read something on Reddit or Twitter. Really, the list goes on. There is one big problem that new investors face. In most cases, it can be hard to know the difference between a good stock and a bad stock. And when they finally buy a stock, they feel anxious, hoping they don’t lose money. But fortunately, there’s a solution that can help you reduce and even remove the anxiety and fear of investing. I would like to introduce you to Tykr, a platform that makes investing easy for anyone, especially beginners. It literally does all the hard work for you. It helps you find safe stocks, and more importantly, it stears you away from risky stocks. We do offer a free trial. Go ahead and visit Tykr. Com. That’s T-Y-K-R.

[00:23:25.650] – Sean

Com. Again, Tykr. Com. All right, back to the show. Well, before we jump to the rapid fire round, is there one key takeaway you can give a parent today?

[00:23:37.590] – Neale

Don’t make money the biggest secret in the household. Talk to the kids, show them a bill. Here’s the electric bill. And by the way, it is directly attached to your behavior. If you talk with the refrigerator open, which takes 30% of the electric bill, you’re wasting money. Let’s come up with energy-saving, electric, just on the electric just onthe electric side that we can do. Maybe we can reduce the thermostat in the winter and raise it in the summer. Maybe we can do other money-saving ideas. And hey, kids, teenagers, I’ll split the savings with you. But you get them involved. You don’t make it a secret. You don’t go out to a restaurant and then hide the bill so they don’t ever know how to calculate a tip. Get them involved. We have made money the biggest secret in the family. It’s ridiculous. Money is the business part of our life. Share it with the kids or don’t be surprised when they get their first credit card and blow it up going, Well, obviously the credit card company thought I was good enough to do this, or they wouldn’t have given me the card. These kids don’t have a clue.

[00:24:52.050] – Neale

Show them how compound interest works in their favor and also to their detriment. Oops, this is going to happen. And just make it part of normal conversation. Same thing with the investing with them. Let them buy stocks they know when they’re 10 years old. Don’t do buying and selling. Do not create day traders.

[00:25:14.390] – Sean

Correct.

[00:25:14.910] – Neale

Buy, hold, and watch and let them buy. I don’t care if it’s Disney or it’s somebody that they know.

[00:25:22.240] – Sean

Yes.

[00:25:22.990] – Neale

And let them start researching. Wow, who knew that they owned ESPN? Who knew? And why did they buy all those other things? Because something could happen and people aren’t going to go to the parks. Okay, this makes sense. Now you’re involving the kids in the way business works. Yeah.

[00:25:45.060] – Sean

At a young age, that’s critical. I love it. Cool. All right, Neil, let’s jump to the rapid-fire round. This is the part of the episode where we get to find out who you really are. If you can, try to answer each question in 15 seconds or less. Are you ready? All right. What is your favorite podcast?

[00:26:02.010] – Neale

I really like the daily news. I love that. I like, Boom! I want to know what’s going on, so I’m not the big stupid when I leave the house.

[00:26:11.420] – Sean

All right. What is a recent book you read and would recommend?

[00:26:15.370] – Neale

Oppenheimer, loved it. Oh, my God, read it.

[00:26:18.960] – Sean

Yeah. I’m thinking of the movie right away, Christopher Nolin, this summer. All right. On that note, what’s your favorite movie?

[00:26:26.400] – Neale

Yeah, I would go back on the Oppenheimer, too. It was… I knew some stuff, but it was pretty earth-shattering in terms of how a person, a time in history, things could totally have been different and also had the people in Germany who were working with Oppenheimer not taking an oath to keep the bomb from Hitler, the world could have been very, very different. That was touched on and brought out in the movie and the book that they kept, that cadre of Jewish scientists kept it from Hitler. It was a freaking miracle that that happened because had he gotten the bomb, I… Yeah.

[00:27:20.060] – Sean

You’re right. It could have been a very different story. Yeah. All right, a few business questions. What is the worst advice you ever received?

[00:27:29.210] – Neale

If you’re a woman, you can’t be a banker.

[00:27:33.440] – Sean

Prove that wrong. All right, put that equation. What is the best advice you ever received?

[00:27:40.460] – Neale

Probably from my mother, which was, no is just a paradigm. It means they don’t understand. And if you believe it, just keep doing it.

[00:27:49.950] – Sean

I love it.

[00:27:51.290] – Neale

Yeah, rejected it. That’s good advice. Who cares? Right.

[00:27:55.240] – Sean

Yeah, keep moving forward. You’ll find a way. This is a fun one, the time-machine question. If you could go back in time to give your younger self advice, what age would you visit and what would you say?

[00:28:06.200] – Neale

I think what I’ve lived my life doing and not being afraid and being thrown out there and doing it. I think in terms of my younger self, I think actually when I joined Chase Manhattan Bank and I heard the words investment banker and had no idea what they were, what that was, and went and spoke to people who were, I somehow thought I wasn’t in some way probably smart enough or good enough. I would say to that younger self, What? Yeah. You can.

[00:28:43.190] – Sean

Figure this out.

[00:28:44.210] – Neale

You got this. Yeah, you got this one. It doesn’t matter that you didn’t go to Harvard Business School. In fact, you’re smarter than they are, so just go do it.

[00:28:53.200] – Sean

Love it. All right. And where can the audience reach you?

[00:28:57.650] – Neale

There’s neelgautry. Com is my website, and they can post things. I love to hear from people and what’s going on. I’m sure they can do it through you and make sure that they’re working with you to really learn to earn, save, spend and share. We need to do this together. I’m thrilled to be here. Thank you.

[00:29:20.490] – Sean

It’s a team effort. Well, thank you so much for your time. Really appreciate what you’re doing. I’ll get all the right links down below in the show notes. But again, thanks for joining me. This is great. Thank you. All right, Neil. We’ll see you. Hey, I’d like to say thank you for checking out this podcast. I know there’s a lot of other podcasts out there you could be listening to, so thanks for spending some time with me. And if you have a moment, please head over to Apple Podcast and leave a five star review. The more reviews we get, especially five star reviews, the higher this podcast will rank in Apple. So thanks for doing that. And remember, this show is for entertainment purposes only. If you heard any stocks mentioned on this podcast, please do not buy or sell those stocks based solely on what you hear. All right, thanks for your time. We’ll see you.